Why is the Mandatory Right to Appraisal in Texas So Important?

by Robert L. McDorman

Dear Mr. McDorman,

I own and operate a collision facility in North Texas. I, like your questioning reader last month, have referred many clients to you over the years, and you were able to help each one resolve the loss dispute with their insurance carrier without the carrier refusing the Right to Appraisal. Each client we have referred to you with under-indemnification and policy coverage issues has come away delighted with the ultimate outcome. I have seen how you are working diligently to help get a mandatory appraisal bill passed in Texas. Thank you!

It was alarming to hear that Progressive and Home State County Mutual filed a policy change request with the Texas Department of Insurance (TDI) to remove the insured’s Right to Appraisal on a repair procedure dispute. Are there any updates on this you can share with the readers? Can you also share some statistics on how long these claims are taking to resolve and the average under-indemnification in repair procedure and total loss claims with the readers? I believe these statistics would help all interested parties understand how vital the mandatory appraisal bill is and why certain insurance carriers are trying to remove the Right to Appraisal for repair procedure disputes from their insurance policy (like State Farm was successful at doing).

Thank you for your comments and questions. As I wrote in the May issue and the previous several months, Progressive and Home State County Mutual Insurance have submitted policy change applications to the TDI requesting approval to remove the Right to Appraisal for repair procedure disputes from their policies. Many general agencies write coverage under Home State County Mutual. I understand that Progressive and Home State County Mutual later rescinded their application requests with this modification in May when it became apparent they would not be approved at this critical point in time.

Thank you for your comments and questions. As I wrote in the May issue and the previous several months, Progressive and Home State County Mutual Insurance have submitted policy change applications to the TDI requesting approval to remove the Right to Appraisal for repair procedure disputes from their policies. Many general agencies write coverage under Home State County Mutual. I understand that Progressive and Home State County Mutual later rescinded their application requests with this modification in May when it became apparent they would not be approved at this critical point in time.

Regarding your questions related to the statistical data we harvest, I have posted below the average results we have achieved for our clients who have come to us for help with the under-indemnification of their repair procedure loss. These averages do not include the hundreds of claims we have moved to the judicial process. These numbers are only for claims where we have invoked the Right to Appraisal for our clients, and the insurance carrier honored this contractual policy right to resolve the dispute.

First, the average timelines for Texas repair procedure appraisal claims that did not go to litigation:

• Date of Loss to Filed Right to Appraisal: 99 days

• Filed Right to Appraisal to Date Carrier Appraiser Appointed: 70 days

• Date Carrier Appraiser Appointed to Date Settled Right to Appraisal: 103 days

Next, average results from these repair procedure appraisal claims:

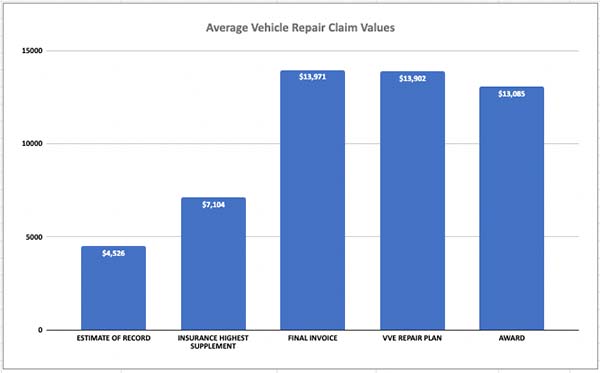

• Average Insurance Carrier Estimate of Record: $4,526

• Average Insurance Carrier Highest Supplement: $7,104

• Average Collision Facility Final Invoice: $13,971

• Average Vehicle Value Experts Repair Plan: $13,902

• Average Right To Appraisal Award: $13,085

TEXAS REPAIR PROCEDURE NON-LITIGATION UNDER-INDEMNIFICATION GRAPH

Under-indemnification in repair procedure claims in Texas is rampant. Most of the above-referenced averages on estimates and supplements had many overlooked (by design) safety and OEM-required operations needed to restore the loss vehicle to its pre-loss condition to the best of one’s human ability. Besides the higher settlements we have obtained for our clients with repair procedure disputes, we have increased total loss settlements on average by $4,200 or 28 percent above the carrier’s proposed final offer. These under-indemnification percentages are staggering and harmful to Texas citizens. I believe limiting or removing the insured’s Right to Appraisal of a repair procedure is a safety issue. The limiting or eliminating of the Right to Appraisal by the insurance carrier in a repair procedure dispute will be the nail in the coffin for safe roadways in Texas.

As I have often said, appraisal is the guardrail for indemnification of the loss when a dispute arises between the insurer and the insured. Without legislation requiring mandatory time-sensitive appraisal rights, we can expect to see continued efforts by all insurers to limit or remove economic relief for the insured when it comes to under-indemnification of a covered loss. In this respect, the insurance carrier can best be seen as a mama bear protecting her cubs and willing to fight anyone trying to take them away. Once they see the insured getting some economic relief for their loss, they quickly act to prevent the insured from getting such relief. Mandatory Right to Appraisal would stop this atrocity. Legislators should come together and pass the mandatory Right to Appraisal bill and put a stop to this before it gets out of hand.

Until legislators pass laws to make the Right to Appraisal mandatory in Texas for all motor vehicle policies, we have no choice but to continue to advise our clients who have been harmed and cheated by their insurance carriers to fight like the third monkey in line to get onto Noah’s Ark when it has already begun to rain, and we will help. In my professional opinion, the more times these systematic under-indemnification schemes are exposed and monetary punishment is levied, the quicker change will come to help us all.

Our position at Auto Claim Specialists is that the Right to Appraisal should be a mandatory contractual right in every policy. For the 89th Texas Legislative panel, we will team up with our lobbyist, Andrew “Drew” Graham, to educate lawmakers and help us secure mandatory contractual appraisal rights for all insured Texans. We, the insureds, are many, and I am confident that if we join forces and all do what we can, we can be successful in securing our rights and our children’s rights to contest insurance settlement offers that would result in underpayment of losses and/or shoddy and dangerous repairs.

The spirit of the Appraisal Clause is to resolve loss disputes fairly and to do so in a timely and cost-effective manner. Invoking the Appraisal Clause removes inexperienced and biased carrier appraisers and claims handlers from the process, undermining their management’s many tricks to undervalue the loss settlement and under-indemnify the insured. Through the Appraisal Clause, loss disputes can be resolved relatively quickly, economically, equitably and amicably by unbiased, experienced, independent third-party appraisers as opposed to more costly and time-consuming methods, such as mediation, arbitration and litigation.

In today’s world, regarding motor vehicle insurance policies, frequent changes in claim management and claim handling policies and non-standardized GAP Addendums, we have found it is always in the best interest of the insured or claimant to have their proposed insurance settlement reviewed by an expert before accepting. There is never an upfront fee for Auto Claim Specialists to review a motor vehicle claim or proposed settlement and give their professional opinion as to the fairness of the offer.

Please call me should you have any questions relating to the policy or covered loss. We have most insurance policies in our library. Always remember that safe repair is a quality repair and quality equates to value. I thank you for your question and look forward to any follow-up questions that may arise.

Sincerely,

Robert L. McDorman

Want more? Check out the July 2024 issue of Texas Automotive!